CFTC may gain broader crypto oversight as staff who questioned major firms were reportedly sidelined

CFTC crypto oversight is moving toward a larger role under the CLARITY Act, but the agency that Congress may soon ask to police much of the US crypto market is facing a more immediate test of its own independence.

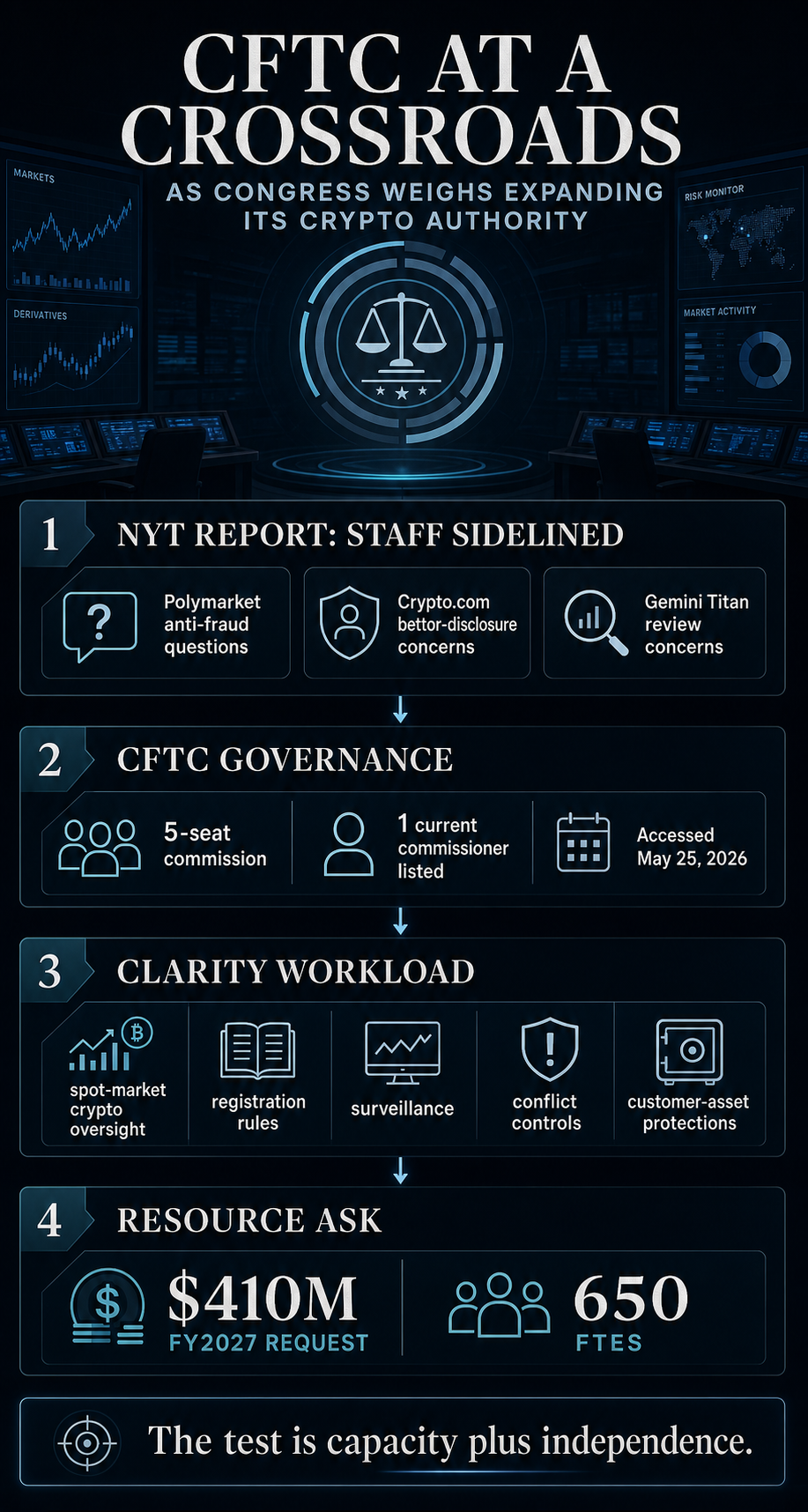

A New York Times investigation reported that senior Commodity Futures Trading Commission officials who raised concerns about Polymarket, Crypto.com, and a Gemini-linked prediction-market plan were suspended, investigated, pushed out, or cut out of relevant discussions as agency leaders helped those firms secure favorable regulatory outcomes.

That report lands directly on top of Washington’s crypto market-structure fight and the broader debate over CFTC crypto oversight. The CLARITY Act would shift a large part of spot-market crypto oversight toward the CFTC, turning an agency already known for lean staffing into the likely federal watchdog for exchanges, intermediaries, surveillance rules, conflict controls, and customer-asset protections.

CryptoSlate recently reported that the bill would put the CFTC’s crypto capacity to the test. The Times report adds a harder test: whether the agency has the internal independence to use that capacity against politically connected firms.

CFTC crypto oversight may expand as internal checks shrink

The CFTC was already a complicated fit for the next phase of CFTC crypto regulation because its historic remit is derivatives, while CLARITY would push it deeper into day-to-day spot crypto supervision.

The bill would force the agency to write rules, register new market participants, monitor trading, police conflicts, and build enforcement capacity around a market far larger and faster than its traditional futures-and-swaps base.

That would make the CFTC under the CLARITY Act the central gatekeeper for much of the market’s federal rulebook.

The agency is asking for more resources. Its FY2027 budget request seeks $410 million and 650 full-time equivalents.

That is real money for a small regulator, but resources alone do not answer the institutional risk now facing the CFTC.

The commission’s own current commissioners page, accessed May 25, says the CFTC is structured as a five-commissioner body and lists Michael S. Selig as chairman under the current commissioners section.

In practice, that leaves unusually concentrated authority at the top while the agency is expected to decide how aggressively it will supervise crypto exchanges, prediction markets and the firms trying to merge the two.

A single listed commissioner is no proof of capture. It does mean fewer visible checks inside the body, Congress may soon rely on to convert crypto legislation into real market oversight. That makes CFTC independence a market-structure issue rather than an internal personnel dispute.

For prediction market regulation, the timing is significant because the Times report describes three matters where CFTC career staff raised concerns. Public records and prior CryptoSlate coverage show why those firms carry relevance beyond the personnel dispute.

| Company | Public regulatory or business record | Credibility test raised |

|---|---|---|

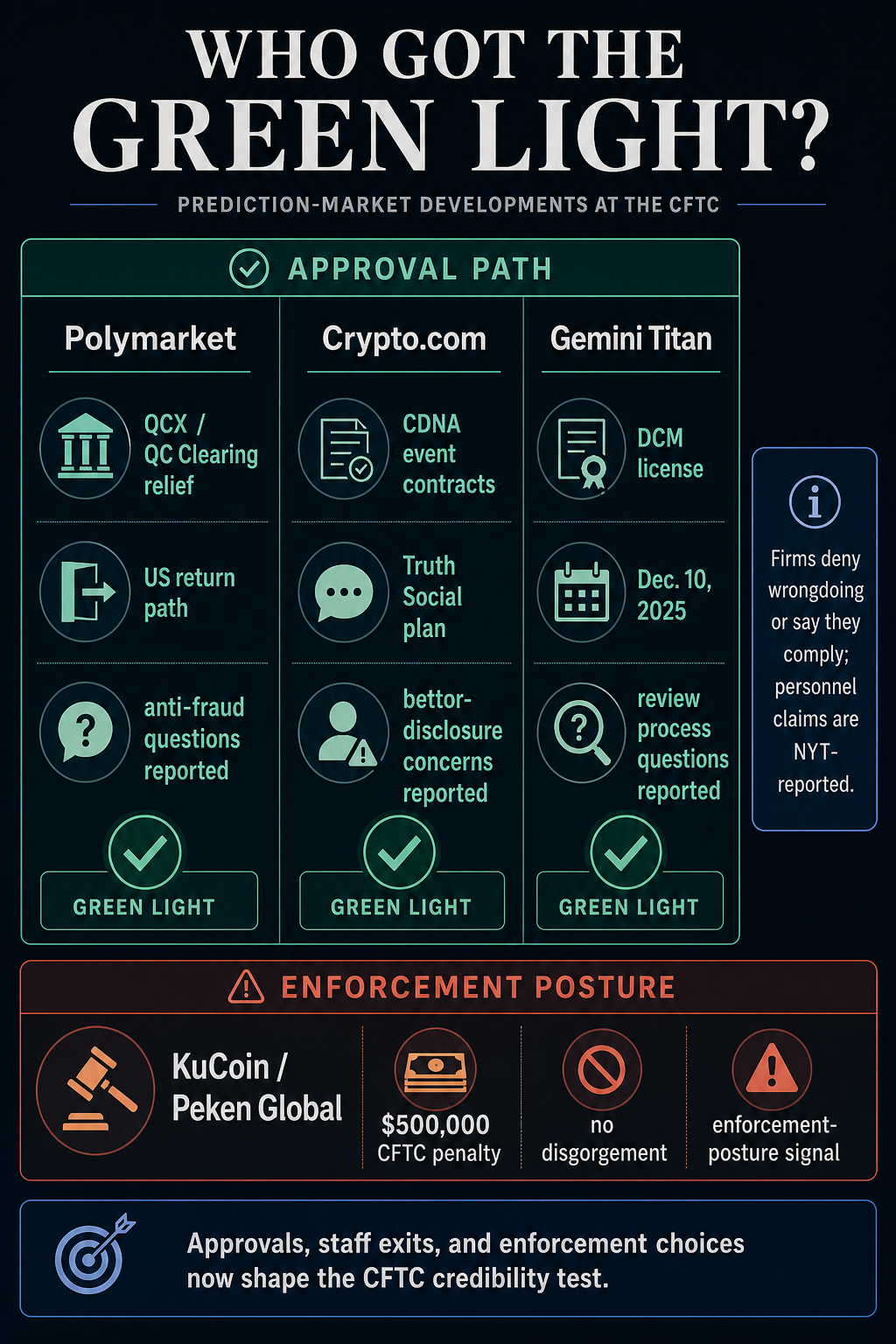

| Polymarket | CryptoSlate reported that Polymarket’s CFTC approval path ran through QCX/QC Clearing no-action relief after its earlier US settlement, and that Donald Trump Jr. joined its advisory board amid a 1789 Capital investment. | The Times reported that staff questioned Polymarket’s anti-fraud protections before the firm received approval and a senior official was later placed on leave. |

| Crypto.com | Trump Media announced that Truth Social would offer prediction markets through an exclusive arrangement with Crypto.com Derivatives North America, which the release described as a CFTC-registered exchange and clearinghouse. | The Times reported that staff worried the firm was giving large trading companies an edge over smaller sports bettors without full disclosure, and that those staffers were cut out of discussions. |

| Gemini Titan | Gemini said its affiliate received a CFTC Designated Contract Market license on Dec. 10, 2025, allowing it to offer prediction markets to US customers. | The Times reported that a draft approval memo came from senior counsel Brigitte Weyls while the staff review was still underway; Weyls later joined Gemini Titan as general counsel. |

The pattern carries more weight than any single row. The record summarized here does not find that Polymarket, Crypto.com or Gemini committed misconduct.

Polymarket told the Times it had strong safeguards, Crypto.com said it complies with federal regulations, and Gemini did not respond to the paper’s questions. The public-policy test is whether career staff can press uncomfortable questions when the firms seeking approval are connected to powerful political and business interests.

KuCoin is a separate enforcement-posture signal rather than a prediction-market approval story. The CFTC’s March 2026 release says Peken Global, operator of KuCoin, was ordered to pay a $500,000 civil monetary penalty, faced an injunction tied to US access without FBOT registration, and was not ordered to pay disgorgement.

The Times reported that Pham wanted staff to drop the case and that the final penalty was far below what agency lawyers had expected.

Capacity is now an independence problem

Before the Times investigation, the main CFTC crypto oversight concern around CLARITY was operational. A new crypto spot-market regime would need registrant categories, surveillance systems, recordkeeping standards, customer-asset rules, conflict controls, conduct rules and enforcement staff.

That is a heavy buildout for an agency whose budget and headcount have always been modest compared with the Securities and Exchange Commission.

After the Times report, the risk is broader. If CFTC enforcement staff who question crypto and prediction-market firms conclude that doing so may put their jobs at risk, then the number of full-time equivalents becomes less important than the incentives around those employees.

An agency can hire staff and still lose oversight capacity if experts avoid hard questions.

That is where prediction markets make the story more concrete for crypto readers. These markets have moved beyond a side curiosity for political gamblers.

They sit at the intersection of crypto rails, sports-style consumer behavior, event contracts, market surveillance and federal-versus-state jurisdiction fights. CryptoSlate has covered the CFTC’s stated focus on the insider problem in prediction markets, a concern that becomes more consequential if the officials responsible for market integrity lose influence inside the agency.

A regulator that cannot credibly question anti-fraud controls, trader advantages or customer safeguards is a problem for both crypto users and traditional market participants. The same supervisory gaps that let a prediction-market venue grow faster can also shape how spot crypto exchanges and intermediaries behave under a new federal regime.

The CFTC’s leadership and the firms involved have a different explanation for the shift. According to the Times, Selig said the agency had gone too far during the Biden administration by turning minor violations into court cases, and that enforcement remains focused on serious fraud, manipulation, abuse and insider trading.

The White House denied conflicts of interest, and the CFTC declined to discuss specific personnel matters or case handling.

That counterargument deserves space. Enforcement agencies do change priorities between administrations, and abandoned investigations can reflect weak evidence, resource choices or parallel proceedings rather than favoritism.

A regulator can also decide that innovation should not be blocked by default.

But the CFTC’s public posture now has to carry more weight than ordinary policy change. The Times reported that the agency brought only two digital-currency cases in the second Trump era, both against individual operators rather than larger firms, and one prediction-market case against an individual accused of insider trading.

That record sits beside the staff-sidelining allegations, the single-current-commissioner structure, the Trump Media-Crypto.com partnership, Gemini’s political backstory and Polymarket’s return to the US market.

Taken together, those facts make CLARITY’s CFTC bet harder to defend on capacity grounds alone. The bill’s supporters can argue that the agency is a better home for crypto market supervision than the SEC.

The tougher test is whether Congress is giving that authority to an agency that can push back against the firms most eager to benefit from it.

What would change the assessment next

The next stage is institutional.

If the White House fills the commission, if the CFTC hires and retains enforcement staff, if conflict rules arrive with teeth, and if the agency brings major-firm cases where the facts justify them, the capture argument becomes harder to sustain.

A focused CFTC could still become a serious crypto regulator if it pairs innovation policy with visible independence.

If the agency stays concentrated in one chair, if career staff continue to exit, if enforcement remains centered on individuals while large firms get approvals, and if CLARITY moves forward without safeguards for vacancies, conflicts and supervision, the risk looks different.

In that scenario, crypto’s new market cop would be gaining power at the same moment its internal checks appear weakest.

That is why the Times report changes the CFTC crypto oversight debate around CLARITY. The test has shifted from whether the CFTC has enough people to regulate crypto to whether those people will be free to ask the questions that shape oversight when the firms across the table have powerful friends.

Credit: Source link