The Federal Reserve Intervenes: Bank Term Funding Program

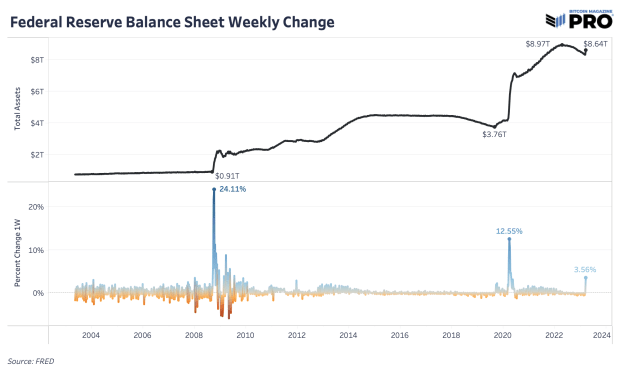

The Federal Reserve balance sheet increased by $300 billion in one week, leading to debate about whether these actions qualify as quantitative easing.

The article below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

The Lender Of Last Resort

Just days after the fallout from Silicon Valley Bank and the establishment of the Bank Term Funding Program (BTFP), there’s been a significant rise in the Federal Reserve’s balance sheet after a full year of decline via quantitative tightening (QT). The PTSD from extensive quantitative easing (QE) is causing many people to sound the alarms, but the changes in the Fed’s balance sheet are a lot more nuanced than a new regime shift in monetary policy. In absolute terms, it’s the largest increase in the balance sheet we’ve seen since March 2020 and in relative terms, it’s an outlier that’s catching everyone’s attention.

The key takeaway is that this is much different than the QE spree of asset buying and the stimulative easy money with near-zero interest rates that we’ve experienced over the last decade. This is about select banks needing liquidity in times of economic distress and those banks getting short-term loans with the goal of covering deposits and paying the loans back in quick fashion. It’s not the outright purchase of securities to indefinitely hold on the balance sheet from the Fed, but rather balance sheet assets that should be short-lived while continuing QT policy.

Nonetheless, it is a balance sheet expansion and a liquidity increase in the short-term — potentially just a “temporary” measure (still to be determined). At the very least, these liquidity injections help institutions not become forced sellers of securities when they otherwise would be. Whether that’s QE, pseudo QE, or not QE is besides the point. The system is showing fragility once again and the government has to step in to keep it from facing a systemic risk. In the short-term, assets that thrive on liquidity increase, like bitcoin and the Nasdaq which have ripped higher at the exact same time.

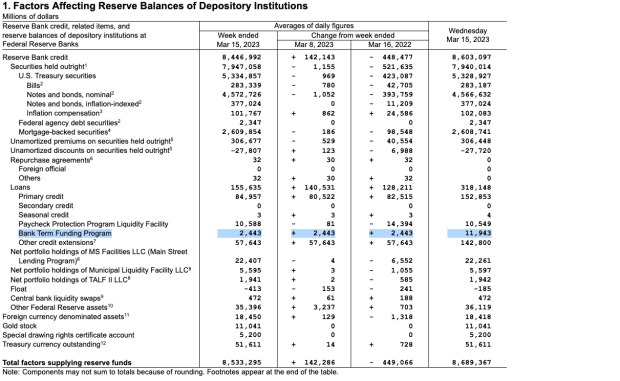

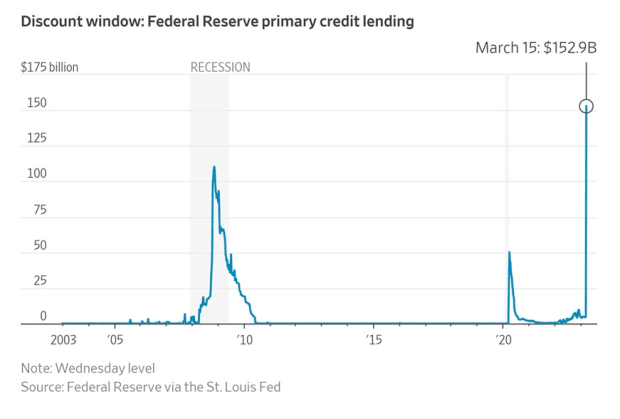

This specific increase of the Fed’s balance sheet is due to a rise in short-term loans across the Fed’s discount window, loans to FDIC bridge banks for Silicon Valley Bank and Signature Bank and the Bank Term Funding Program. Discount window loans were $152.8 billion, FDIC bridge bank loans were $142.8 billion and BTFP loans were $11.9 billion for a total of over $300 billion.

The more alarming increase is in the discount window lending as that is a last resort, high cost liquidity option for banks to cover deposits. It was the largest discount window borrowing on record. Banks using the window are kept anonymous as there is a legitimate stigma issue from finding out who’s in need of short-term liquidity.

This brings back recent memories of the 2019 emergency liquidity injection and intervention by the Fed into the repo market to stabilize cash demand and short-term lending activities. The repo market is a key overnight financing method between banks and other institutions.

Download the FREE “Banking Crisis Survival Guide” Today!

Get your copy of the full report here.

The Upcoming FOMC Meeting

The market is still expecting a 25 bps rate hike at the FOMC meeting next week. All-in-all, the market turmoil so far hasn’t proven to “break enough things” yet, which would require an emergency pivot from central bankers.

On its path to bringing inflation back to the 2% target, month-over-month Core CPI was still increasing in February while initial jobless claims and unemployment haven’t budged much. Wage growth, especially in the services sector, still remains fairly strong at the 3-month annualized rate of 6% growth last month. Although slightly coming down, more unemployment is where we will have to see more weakness in the labor market in order to take wage growth much lower.

We’re likely far from the end of the chaos and volatility this year,as each month has brought new levels of uncertainty in the market. This was the first sign of the system needing Federal Reserve intervention and swift action. It likely won’t be the last in 2023.

That concludes the excerpt from a recent edition of Bitcoin Magazine PRO. Subscribe now to receive PRO articles directly in your inbox.

Relevant Past Articles:

- Banking Crisis Survival Guide

- PRO Market Keys Of The Week: Market Says Tightening Is Over

- Largest Bank Failure Since 2008 Sparks Market-Wide Fear

- Banking Troubles Brewing In Crypto-Land

- A Tale of Tail Risks: The Fiat Prisoner’s Dilemma

- The Bank Of Japan Blinks And Markets Tremble

- The Everything Bubble: Markets At A Crossroads

- Silvergate Bank Faces Run On Deposits As Stock Price Tumbles

- Counterparty Risk Happens Fast

- Not Your Average Recession: Unwinding The Largest Financial Bubble In History

Credit: Source link